Open and Closed Loop Payment Systems

Unveiling the Power of Open and Closed Loops

Welcome to The Engineer Banker, a weekly newsletter dedicated to organizing and delivering insightful technical content on the payments domain, making it easy for you to follow and learn at your own pace

Payment systems across the globe are categorized into two broad types: open loop and closed loop systems. These classifications are based on the system's structure and the degree of interoperability between different entities within the payment ecosystem.

Open Loop Payment Systems

An open-loop payment system is characterized by its broad interoperability, where a transaction involves at least four entities: the cardholder, the merchant, the issuer (usually a bank that provides the card to the cardholder), and the acquirer (usually a bank that services the merchant). An excellent example of an open-loop system is a credit card network, like Visa or MasterCard also known as open-loop cards.

In an open-loop system, a cardholder can use their Visa card, issued by any bank, at any merchant that accepts Visa worldwide. Visa, as the network, facilitates the transaction between the issuing bank and the acquiring bank.

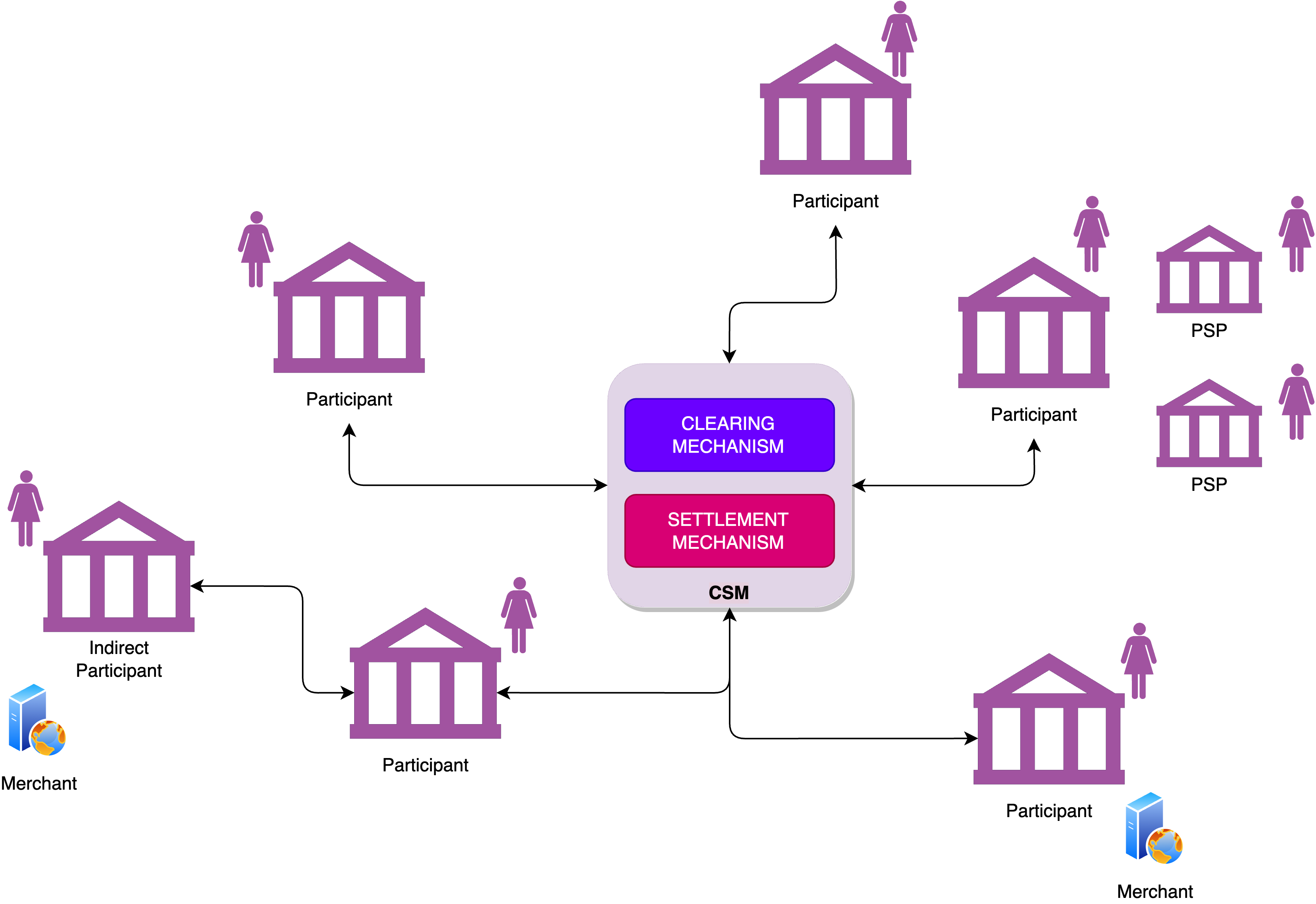

In open-loop payment systems, transactions are characterized by a meticulously structured pathway that ensures smooth fund transfers between parties even if they don't bank with the same financial institution. The process commences when a party, which could be an individual or a business, initiates a payment through their bank. This bank, in turn, interacts with the payment system which acts as a conduit to route the funds to the recipient's bank. The recipient's bank then credits the funds to the recipient, completing the transaction. This framework is advantageous as it negates the need for banks to maintain direct relationships with each other. Upon joining an open-loop payment system, a bank is instantaneously connected to a vast network, enabling it to engage in transactions with all other participating banks, and the reciprocal is equally true. This inherent aspect of open-loop systems underpins their ability to scale expeditiously.

Further, in an open-loop arrangement, end parties - individuals or businesses - can send funds to each other regardless of whether they hold accounts with the same bank. Essentially, all participants are interconnected through the payment system and the banks that act as intermediaries.

It is crucial to recognize that banks participating in an open-loop payment system are governed by a set of rules. However, as these banks operate as independent entities, they each have distinct projects and timelines for the implementation of these rules. Generally, the window for compliance can span several months, and in certain cases, years. One of the intrinsic limitations of open-loop models is that the adoption of new rules can be protracted. Additionally, there is a possibility for differing interpretations of the same rule by various banks, leading to diverse implementations.

Prominent examples of open-loop systems include Visa and MasterCard. If you hold a credit or debit card from either of these brands, it is important to understand that the card was issued by your bank and not directly by Visa or MasterCard. In this scenario, your bank acts as an intermediary between you and the payment systems. Similarly, merchants who accept Visa or MasterCard don't engage directly with these payment networks; instead, they enter into agreements with banks that are members of the Visa or MasterCard networks. This underscores the pivotal role that banks play as intermediaries in open-loop systems, bridging the gap between end parties and the payment networks.

In the dynamic and interconnected world of financial transactions, banks frequently establish connections with multiple open-loop systems to facilitate a diverse range of payments. These open-loop systems can be categorized into domestic or national systems, and international systems, each serving a distinct purpose and clientele.

In France, as in many other countries, banks are known to connect to various domestic open-loop systems. One of the most notable domestic systems in France is the “Système Interbancaire de Télécompensation” (SIT), which is an interbank payment system. SIT mainly processes cheques, direct debits, and credit transfers within France. Being part of this system allows banks to efficiently handle a plethora of internal transactions, catering to the everyday needs of individuals and businesses alike.

Furthermore, France is part of the Single Euro Payments Area (SEPA), which is an integration initiative by the European Union to harmonize electronic euro payments across Europe. This means that banks in France are also connected to this regional open-loop system, allowing customers to make credit transfers, direct debits, and card payments throughout the European Economic Area as effortlessly as domestic transactions.

Moving to international open-loop systems, French banks are invariably connected to global networks like SWIFT (Society for Worldwide Interbank Financial Telecommunication). SWIFT is an international messaging network used by financial institutions to securely send and receive information, such as money transfer instructions. French banks leverage SWIFT for transactions that transcend European borders, enabling global trade and individual cross-border transactions.

Additionally, French banks are linked to international card networks such as Visa and MasterCard. These open-loop systems enable French citizens to use their debit or credit cards across the globe. For example, a tourist from France can use their Visa card to make purchases in the United States or anywhere else where Visa is accepted.

In summary, by being connected to multiple open-loop systems, both domestic and international, banks in France can offer their customers a comprehensive range of payment options. This multiplicity in connections equips the banks with the ability to process varying kinds of payments – from local transactions in rural France to large-scale international money transfers – thereby supporting the multifaceted financial requirements of individuals and businesses operating in an increasingly globalized economy.

Pros of Open Loop Systems

Ubiquity: Open-loop cards, like those issued by Visa or MasterCard, are accepted by millions of merchants worldwide, offering unparalleled convenience and usability.

Flexibility: They provide flexibility in terms of the variety of transactions that can be carried out, such as ATM withdrawals, online purchases, and point-of-sale transactions.

Rewards and Incentives: Many open-loop cards come with rewards and benefits like cashback, air miles, and more.

Cons of Open Loop Systems

Fees: Because open-loop systems involve multiple parties, they often come with higher fees, impacting both merchants (transaction fees) and consumers (annual fees, interest rates).

Dependence on Banks: The system's operation heavily relies on banks, thus excluding unbanked or underbanked populations from its benefits.

Closed Loop Payment Systems

Contrastingly, closed-loop systems, also known as proprietary systems, involve transactions between two parties within the same system. One classic example of a closed-loop system is a store gift card, such as a Starbucks card. The card is issued by Starbucks, accepted only at Starbucks locations, and the transaction is wholly managed by Starbucks. In closed-loop systems, customers are required to have an account within the system to carry out transactions. This arrangement is akin to operating within an exclusive ecosystem where the financial operations are confined to the participants registered within that specific platform. Such systems are prevalent in various marketplaces and financial service providers.

One classic example of a closed-loop system is PayPal. PayPal allows users to create an account, which they can fund through a bank account or credit card. Once the account has funds, the user can transact with any other PayPal user or merchant that accepts PayPal payments. Essentially, the transaction occurs within the PayPal ecosystem, and for someone to send or receive money through PayPal, having an account is a prerequisite.

Amazon, the giant online marketplace, also operates a form of closed-loop system through Amazon Pay. Customers can use Amazon Pay to make purchases from Amazon and other participating retailers. Funds in the Amazon Pay account can be used exclusively within the network of merchants that accept Amazon Pay, thereby creating a closed ecosystem

Another interesting implementation of closed-loop payment systems is seen in the public transit sector. Cities like London and Hong Kong have leveraged closed-loop systems for their Oyster and Octopus cards, respectively. Recently, however, there's a trend towards transitioning to open-loop systems for public transit to allow commuters to use their credit or debit cards directly, without the need for a separate transit card.

Although closed-loop systems are typically associated with a more contained scope due to their inherent structure, which usually limits transactions within a specific company's ecosystem, there are remarkable instances where they have transcended these bounds and evolved into large-scale national infrastructures. This expansion rivals the size and reach of some open-loop systems, creating vast, comprehensive networks that transform the dynamics of the national payments landscape. Two salient examples of this phenomenon are WeChat Pay and Alipay in China. These digital payment platforms, initially launched to support transactions within their respective apps, have expanded massively. They now serve hundreds of millions of users across the nation, supporting a wide array of transactions beyond their initial ecosystems. From utility bills to in-store purchases, and even peer-to-peer transactions, these closed-loop systems have demonstrated an exceptional capacity for growth and adaptation.

In LATAM a major example is Mercado Pago, the payment platform of Mercado Libre, started as a closed-loop system, as it was originally designed to facilitate transactions within the Mercado Libre marketplace. However, it has since expanded beyond this scope and now functions more like an open-loop system.

Mercado Pago now allows users to store money in a digital wallet, make purchases at a variety of online and physical stores not associated with Mercado Libre, and even make peer-to-peer transactions. Users can also fund their Mercado Pago account from various sources and withdraw money to a bank account. Furthermore, Mercado Pago offers its own credit card, further enhancing its open-loop capabilities.

Therefore, while it began as a closed-loop system within the Mercado Libre marketplace, Mercado Pago has evolved to provide services typical of an open-loop payment system, broadening its utility for users.

Pros of Closed Loop Systems

Control: Since the issuer has complete control over the system, they can tailor the user experience and manage the transaction costs more effectively.

Lower Costs: Transaction costs are typically lower in closed-loop systems as they avoid interchange fees associated with open-loop systems.

Customer Engagement: These systems can drive customer loyalty and repeated business, as the payment instruments are only usable within a particular ecosystem.

Reduced technical complexity: Given that payments in a closed-loop system fundamentally constitute an internal payment in the form of a booking, they are significantly easier to implement.

Cons of Closed Loop Systems

Limited Acceptance: Closed-loop cards can only be used within a specific network or retailer, limiting their versatility.

Lack of Competition: The absence of competition within the system can lead to monopolistic practices, potentially impacting pricing and service quality.

As the global payment landscape continues to evolve, understanding these systems' respective benefits and limitations can inform better strategies for businesses, financial institutions, and policymakers alike, ensuring the creation of inclusive, efficient, and consumer-friendly payment ecosystems.