Payments Infrastructure Anatomy II

Learn the ecosystem behind a payments infrastructure

In Today's article, we will continue discussing the relationship between payments and neighboring functions in a bank or fintech ecosystem. If you missed our previous article we invite you to take a moment to visit it and refresh your understanding of the infrastructure interfaces we discussed in our first installment.

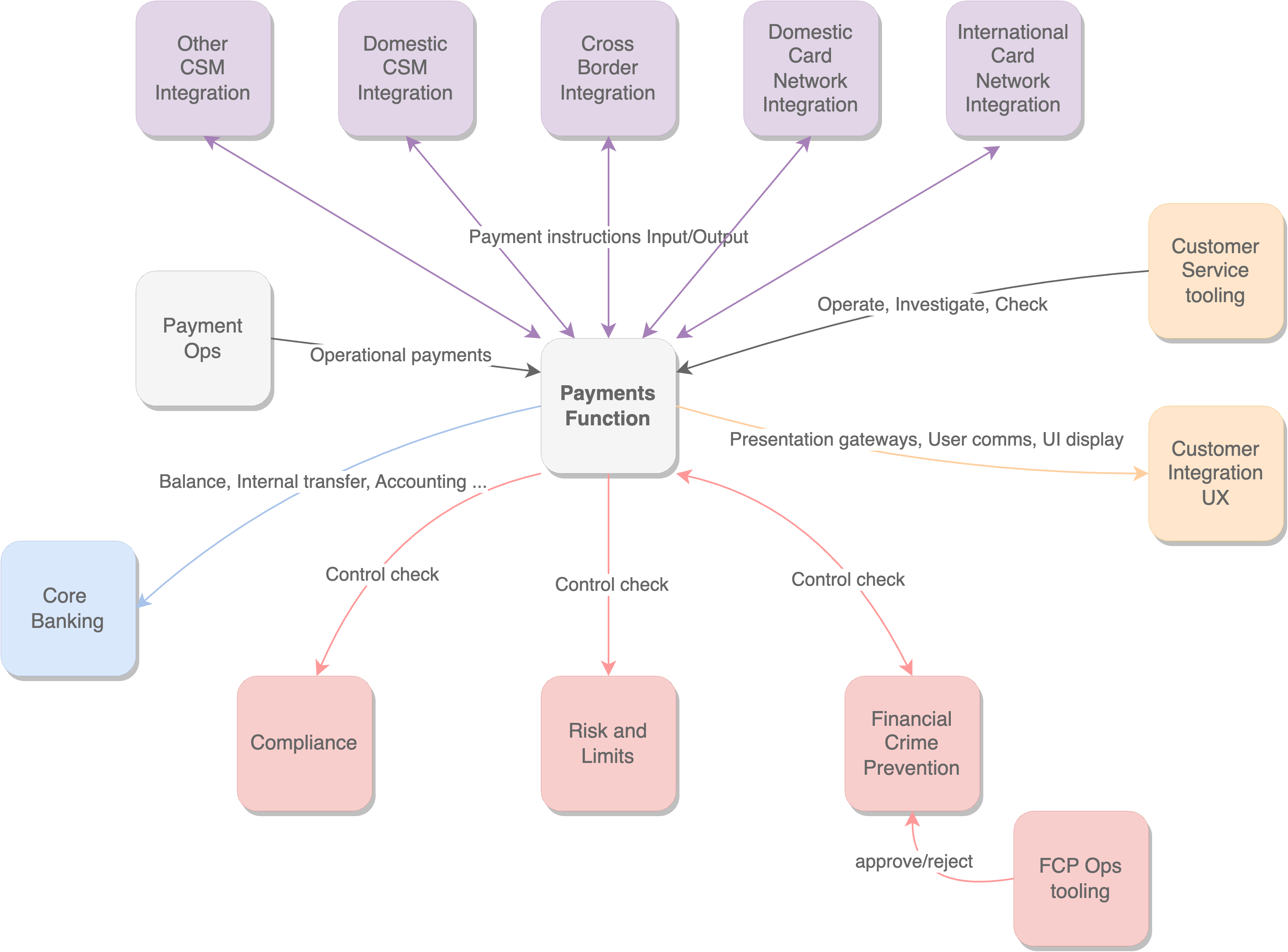

It will provide valuable context as we continue our exploration of the interactions between payments and other key functions in today's article. As we dive deeper into payments infrastructure anatomy, it's important to note the boundaries and functional elements that form the foundation of a payments ecosystem. Let's revisit these boundaries by examining the following diagram and let’s continue with the analysis of those interfaces.

User Experience

It is crucial that a payments infrastructure integrates seamlessly with the customer-facing elements of a bank or fintech ecosystem. This includes interfaces such as mobile apps, online banking platforms, ATMs and other payment access points. Additionally, it is important to consider the type of customers being served and the channels through which they prefer to interact with the payment system.

This seamless integration ensures a cohesive and user-friendly experience for customers across various touchpoints. Take, for example, a mobile banking app that allows users to conveniently initiate payments, check their transaction history, and manage their accounts on the go. By integrating the payments infrastructure with such customer-facing interfaces, banks and fintechs can empower their users with quick and secure payment capabilities at their fingertips. Furthermore, online banking platforms play a vital role in facilitating payment transactions. Customers can effortlessly transfer funds between accounts, pay bills, and set up recurring payments with just a few clicks. The payments infrastructure must seamlessly communicate with these platforms, ensuring smooth and reliable transaction processing.

Let's not forget the ubiquitous presence of ATMs, which serve as essential payment access points for cash withdrawals and balance inquiries. A robust payments infrastructure should seamlessly integrate with ATMs to enable hassle-free cash transactions and provide real-time updates on account balances.

When designing a payments infrastructure, it is essential to consider the diverse needs and preferences of the customers being served and analyse the key payment demands in the market , especially for those banks with a presence across multiple countries or geographies.

This customer-centric approach ensures that the payments offering meets the unique requirements of each demographic and region leading to an optimal payment market fit.

In certain markets, specific payment practices may exhibit a preference for various payment methods such as direct debits, cash transactions, or domestic payment systems. For instance, in countries like Germany, direct debit payments are widely embraced, enabling recurring payments such as utility bills, subscriptions, and insurance premiums to be conveniently deducted from customers' bank accounts. Similarly, in economies with a large unbanked population or limited digital infrastructure, cash remains a dominant form of payment, often relied upon for daily transactions, retail purchases, and person-to-person transfers. Additionally, domestic payment schemes, such as the United Kingdom's Faster Payments Service or India's Unified Payments Interface (UPI), are designed to facilitate fast and secure domestic transactions, enabling individuals and businesses to transfer funds seamlessly within their respective national boundaries. Understanding and adapting to these unique market practices is crucial for organizations to tailor their payment infrastructure effectively and provide optimal payment solutions that align with the specific preferences and habits of their target customers

Customer Service

The payments function plays a significant role in customer service within a bank or fintech organization. It serves as a critical touchpoint where customers interact with the financial institution to initiate, track, and resolve payment-related activities. Customer service teams are responsible for providing support and assistance to customers regarding their payment inquiries, issues, and concerns. When a customer encounters a problem with a payment, such as a failed transaction, incorrect amount deducted, or unauthorized activity, they typically reach out to the customer service department for resolution. Customer service representatives work closely with the payments team to investigate and resolve these issues promptly, ensuring a positive customer experience.

Moreover, customer service teams also assist customers in navigating the various payment channels and platforms offered by the organization. They provide guidance on using digital payment tools and address any usability or technical issues customers may face during the payment process. This collaboration between payments and customer service ensures that customers have a seamless and satisfactory payment experience. In order to facilitate seamless customer service experiences, it is vital for the payments team to equip its customer agents with the most effective and efficient tools available. By providing robust tools, the payments team empowers customer agents to handle payment-related inquiries, resolve issues, and deliver exceptional service.

In addition to issue resolution and technical support, the payments function intersects with customer service in terms of handling inquiries related to payment options, transaction statuses, and payment-related policies. Customer service representatives are equipped with knowledge about the organization's payment offerings, such as different payment methods, payment limits, and transaction processing times. They provide accurate and up-to-date information to customers, helping them make informed decisions and understand the intricacies of the payment ecosystem. Furthermore, equipping customer agents with automation capabilities can significantly streamline processes and enhance service delivery. Automated workflows and intelligent routing systems can route customer inquiries to the most appropriate agent, reducing response times and ensuring that customers receive prompt and relevant assistance. Additionally, self-service portals or knowledge bases can provide customers with immediate access to relevant information, enabling them to find answers to common payment-related questions independently

By aligning the payments function with customer service, organizations can deliver enhanced customer experiences, effectively address payment-related concerns, and build long-lasting relationships with their customers. This collaboration ensures that customers receive personalized and efficient support throughout their payment journey, fostering trust, loyalty, and satisfaction.

Domestic rails integration

The domestic rails are another important component of the payments infrastructure, referring to the electronic systems that facilitate clearing and settlement for domestic transactions. These rails include Automated Clearing Houses, Real-time Gross Settlement systems, and domestic card networks. Overall, the payments function's intersection with domestic card networks is crucial for enabling smooth, secure, and efficient card-based transactions within a specific country. By collaborating with domestic card networks like China UnionPay, RuPay in India, Japan Credit Bureau, Interac (Canada), EFTPOS (Australia and New Zealand) the payments function ensures the seamless functioning of the card payment ecosystem relevant to a particular region, providing consumers and businesses with reliable and convenient payment options within the region.

Connecting to domestic clearing houses within a specific region offers several benefits. Firstly, it enables direct access to local payment infrastructures, streamlining payment processing and reducing dependencies on intermediaries. This results in faster and more efficient transaction settlements, enhancing overall payment speed and customer satisfaction. Additionally, connecting to domestic clearing houses allows for improved risk management and compliance with local regulations, ensuring secure and compliant payment operations. Moreover, it facilitates interoperability with local banks and financial institutions, fostering collaboration and expanding business opportunities within the region. By leveraging domestic clearing houses, organizations can optimize their payment operations, enhance local market reach, and strengthen their position in the regional payment landscape.

Cross border integration

The world is more interconnected than ever before, and businesses and individuals engage in cross-border transactions regularly. By having a robust cross-border payment solution, banks can effectively address the needs and demands of their customers who engage in international trade, travel, or remittance activities. One key benefit of incorporating a cross-border solution is enhanced customer experience. Customers expect fast, secure, and cost-effective international payments, and banks that offer reliable cross-border solutions can deliver on these expectations. By providing seamless cross-border payment capabilities, banks can attract and retain customers, strengthening their competitive position in the market. Moreover, a cross-border solution allows banks to expand their market reach. It enables them to serve customers engaged in international business activities, such as importers, exporters, and multinational corporations. Incorporating a cross-border solution also promotes operational efficiency within the bank. It enables streamlined processes for handling international transactions, reducing manual intervention, and minimizing errors. Furthermore, compliance and risk management are critical considerations in cross-border transactions. Banks must adhere to international regulations, anti-money laundering (AML) requirements, and sanctions screening to ensure the integrity and security of cross-border payments. In summary, incorporating a cross-border solution in a bank is vital to meet the growing demands of customers engaged in international activities, expand market reach, enhance operational efficiency, and ensure compliance and risk management.

Over the past two articles, we have thoroughly examined the fundamental functional blocks that comprise a robust payments infrastructure in banks and fintech companies. As we move forward in this series, we will embark on a detailed exploration of the interfaces that bind these blocks together, delving into the inner workings of their interactions. Join us in the upcoming installments as we dive deep into the realm of these critical connections.