Technical facilitators

The Unseen Enablers of Financial Transactions

Welcome to The Engineer Banker, a weekly newsletter dedicated to organizing and delivering insightful technical content on the payments domain, making it easy for you to follow and learn at your own pace

The payment landscape is a complex web of various stakeholders, including financial institutions, customers, clearing and settlement infrastructures and regulatory bodies. Among them, technical facilitators serve as the backbone that enables seamless, secure, and efficient payment transactions. Technical facilitators are entities that provide the technological infrastructure and services necessary for processing payments but do not engage in actual clearing and settlement. These can include payment gateways, payment processors, and software service providers. While they might not handle the financial aspects of transactions, their role is crucial for facilitating them. This article explores the role, functionality, and significance of technical facilitators that help banks and financial institutions to connect to ACHs, leaving for another article the discussion of technical facilitators for cards. These technical facilitators provide a comprehensive array of advantages to financial institutions that opt to leverage their specialized services. Beyond merely facilitating seamless payment processing, they act as strategic partners in enabling banks and other financial entities to operate more efficiently, innovate more rapidly, and compete more effectively in a complex and evolving market landscape.

These facilitators offer a variety of capabilities to financial institution that decide to use their services

Friendly APIs and enhanced developer experience

Technical facilitators in the payments industry often opt for RESTful APIs, which have gained significant traction and popularity among modern engineers. This contemporary approach stands in contrast to the more legacy-based XML messaging systems commonly employed by Clearing and Settlement Mechanisms (CSMs) to enable service connectivity. One of the advantages of RESTful APIs is their inherently lightweight and stateless nature, which fosters easier integration and greater scalability compared to their XML-based counterparts.

Moreover, these RESTful APIs are often accompanied by comprehensive, well-organized documentation. This is a critical asset for engineers who require clarity and detailed guidelines when working on integration or development projects. The documentation typically includes various code samples, use-case scenarios, and troubleshooting tips, thereby facilitating a smoother and more intuitive developmental process.

These companies often help engineering teams in the financial institution to perform the mandatory testing for the required certification prior to joining the payment scheme.

Faster go to market

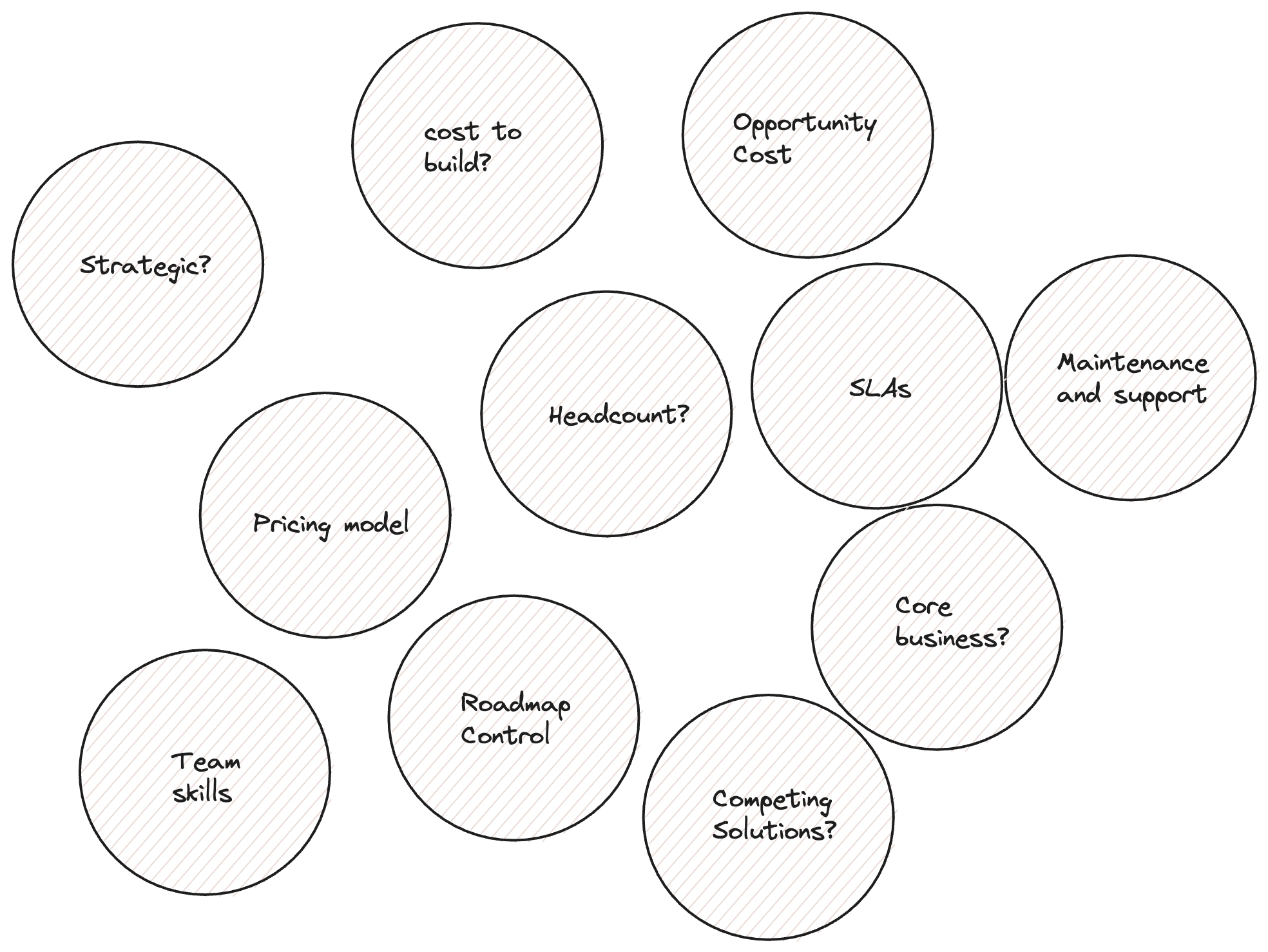

When banks are faced with the 'build vs. buy' decision for integrating with a payment scheme, the 'buy' option typically offers a distinct advantage in terms of speed-to-market. Opting for a direct integration with a payment scheme can often prove to be a cumbersome process. This is largely because it entails navigating through complex protocols, regulatory requirements, and multi-layered systems architecture, all of which can extend the project timeline significantly.

Some elements to consider when facing a build vs buy decision:

On the other hand, partnering with a technical facilitator simplifies the integration journey substantially. These facilitators usually offer pre-built solutions that are designed to align with the payment scheme's requirements, substantially cutting down the time and effort needed to go live. They provide standardized interfaces, often through RESTful APIs, which can be easily adapted to the bank's existing systems.

Moreover, opting for a 'buy' decision via a technical facilitator allows the bank to minimize its upfront technical investment. This can be particularly advantageous for banks that are aiming to expand into new geographical markets or diversify their payment offerings but are constrained by budget limitations or resource availability. Utilizing a technical facilitator's services provides the bank with a plug-and-play solution that is not only more cost-effective but also scalable and adaptable to future changes in payment protocols or regulations.

In addition, choosing to 'buy' usually includes ongoing support and maintenance, reducing the operational load on the bank's internal teams. This allows them to focus on core banking services and other strategic initiatives, rather than being bogged down by the intricacies of payment scheme integration and compliance.

Opting for a technical facilitator in the 'build vs. buy' equation offers a more streamlined, less resource-intensive path to market. It helps banks to expedite their payment scheme integration process while significantly reducing the technical investment and operational complexity involved in initiating and maintaining such a system.

Single point of integration

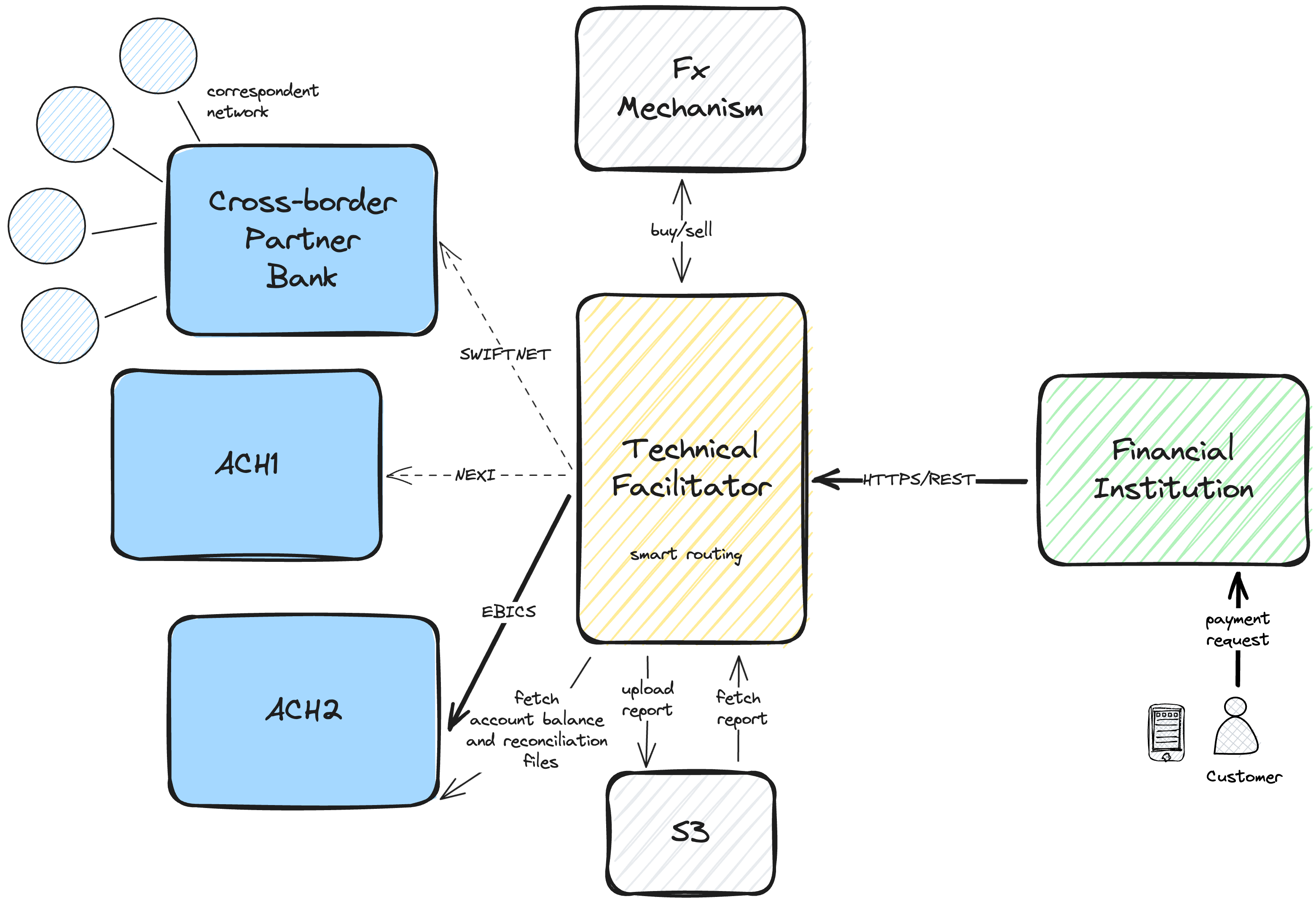

Some of these facilitators offer multiple downstream ACH integrations allowing an institution to connect to a single infrastructure and reducing connectivity infrastructure costs.

Certain technical facilitators in the payments industry provide the advantage of multiple downstream Automated Clearing House (ACH) integrations. This enables financial institutions to streamline their operations by connecting to a singular, unified infrastructure rather than establishing separate connections for each ACH. This consolidation is especially beneficial for institutions looking to optimize their payment processing architecture, as it can significantly reduce the costs associated with maintaining multiple, disparate connectivity infrastructures.

By offering a one-stop-shop for ACH integrations, these technical facilitators make it far easier for financial institutions to navigate the increasingly complex landscape of payments. Instead of dealing with the logistical and technical challenges of individual connections, institutions can focus on fine-tuning their payment strategies and improving their customer experience. This approach often entails less upfront investment, fewer operational headaches, and reduced ongoing maintenance costs.

Furthermore, the single-point connectivity offered by these facilitators allows for quicker implementation of new features and capabilities. It provides a more agile framework, which can be easily scaled or adapted to include additional ACH networks or payment schemes as needed. This flexibility is particularly beneficial for financial institutions looking to expand their market presence or adapt to changing regulatory environments without overhauling their existing payment systems.

Local knowledge and partnerships

These facilitators specializing in payments often bring extensive domain knowledge of both a specific country's regulatory landscape and various payment methods prevalent in that market. This expertise proves invaluable for banks and financial institutions looking to establish a foothold or expand their operations in a new geographical territory. By leveraging the facilitator's localized knowledge and insights, the bank can more efficiently navigate the complexities of regional compliance regulations, consumer payment preferences, and other market-specific nuances.

Furthermore, these facilitators often have well-established relationships with regulatory bodies, local financial institutions, and other key stakeholders in the targeted market. This network can help accelerate the bank's entry into the market by smoothing out potential roadblocks, whether they be regulatory approvals or partnership negotiations. Essentially, the facilitator acts as a market entry enabler, expediting processes that could otherwise take a considerable amount of time and effort.

Moreover, the in-depth understanding that these facilitators have about various payment methods—whether it's mobile payments, electronic fund transfers, or card transactions—can also serve as a strategic asset. They can provide data-driven insights into consumer behavior, emerging payment trends, and market demands, thus enabling the bank to tailor its product offerings more effectively. These insights can inform the bank's strategy, from product development to marketing, making their entry or expansion in the market more aligned with local preferences and needs.

The domain knowledge offered by these facilitators also extends to technical aspects such as payment processing protocols, message formats, and security measures. By relying on their expertise, banks can significantly reduce both the time and costs associated with in-house research, development, and compliance adherence.

Facilitators with specialized domain knowledge offer a multitude of advantages for banks aiming to penetrate a new market. Their expertise streamlines regulatory compliance, provides valuable market insights, expedites partnerships, and ultimately allows the financial institution to build a market presence in a more efficient and informed manner.

Rulebooks and payment landscape evolution

The decision to integrate with a payment scheme should be viewed as a long-term strategic investment, one that extends well beyond the parameters of the initial bootstrap project. Financial institutions must anticipate and plan for numerous variables that are subject to change over time—be it in the form of evolving payment specifications, updates in compliance regulations, or shifts in market practices. Here, the role of a technical facilitator becomes especially critical as they help the bank navigate through these ever-changing landscapes.

Technical facilitators offer the benefit of dedicated expertise in managing compliance requirements, ensuring that banks are continually aligned with updated rules and regulations. This reduces the risk of non-compliance, which could otherwise lead to costly fines and reputational damage. They often possess an in-depth understanding of local, regional, and international regulations, offering a comprehensive view that prepares the bank for virtually any regulatory changes that may arise.

Further, payment schemes are dynamic ecosystems where message formats and transaction rules are subject to change. Technical facilitators not only monitor these changes but also work proactively to update the bank's systems accordingly. This ensures that the financial institution remains compatible with the payment scheme's evolving requirements, thereby maintaining transaction efficiency and integrity.

As market practices evolve, customer expectations and behaviors do too. Technical facilitators can provide valuable insights into market trends and shifts in consumer preferences. This empowers the bank to adapt its services to meet emerging demands, fostering greater customer satisfaction and loyalty in the long run. Facilitators often possess data analytics capabilities that allow them to monitor transaction patterns and customer behaviors, insights that can be invaluable for future strategy and product development.

Moreover, the long-term partnership with a technical facilitator often results in cost savings in the long run. While there is an upfront investment required for integrating with a payment scheme, the ongoing maintenance and adaptation are generally less resource-intensive when managed by a specialized facilitator. This allows the bank to allocate its resources more effectively, focusing on core competencies and strategic initiatives instead of the operational intricacies of payment scheme integration.

Integrating with a payment scheme is a significant, long-term undertaking that involves various dynamic components—from shifting compliance regulations to evolving market practices. A technical facilitator acts as a crucial partner in this journey, providing the expertise and support needed to adapt and thrive in a fluctuating payments landscape.

Value-added services

Certain technical facilitators go above and beyond basic payment processing services to offer a suite of value-added capabilities that can significantly enhance a bank's operational efficiency and strategic flexibility. These extra services often include features such as advanced reconciliation mechanisms, comprehensive reporting tools, smart routing algorithms, and foreign exchange (FX) management systems.

The reconciliation feature streamlines the bank's ability to match transaction records with accounting statements, thereby simplifying the audit process and reducing administrative overhead. Advanced reconciliation tools often leverage machine learning algorithms to identify discrepancies automatically, flagging them for further review and resolution. This can significantly reduce human errors and improve the integrity of the bank's financial records.

Sophisticated reporting capabilities offer financial institutions an in-depth analytical view of their payment transactions. These reports can include various metrics like transaction volumes, failure rates, and performance benchmarks, among others. With such data-driven insights, banks can make more informed decisions on scaling operations, identifying bottlenecks, and optimizing service offerings. Some facilitators even provide real-time dashboards that offer instant access to key performance indicators, enabling swift and proactive management decisions.

Smart routing algorithms are another critical feature offered by select facilitators. These algorithms determine the most efficient and cost-effective path for a transaction, taking into account variables such as fees, speed, and reliability. Such optimization can lead to significant cost savings and improve the customer's experience by speeding up transaction times.

FX management services can be a game-changer for financial institutions that operate internationally. These services often include real-time currency conversion, risk mitigation strategies, and hedging solutions. Advanced FX management tools can automatically select the most favorable exchange rates and execute transactions at optimal moments, thereby maximizing profitability and minimizing exposure to currency market fluctuations.

In essence, these enhanced capabilities offered by technical facilitators serve as strategic assets that empower banks to operate more efficiently, gain competitive advantages, and better meet customer needs. By providing features such as advanced reconciliation, detailed reporting, smart routing, and comprehensive FX management, facilitators offer banks a more holistic, efficient, and adaptable payment processing solution.

As a summary:

Firstly, these facilitators streamline the often cumbersome integration processes, allowing financial institutions to rapidly enter new markets or adopt advanced payment technologies. By doing so, they significantly accelerate time-to-market and reduce the need for extensive internal technical development, thereby mitigating both cost and risk.

Secondly, they offer modular and scalable solutions that can grow in tandem with a financial institution's expanding business needs. This scalability ensures that banks can adapt to increasing transaction volumes or more complex payment architectures without having to overhaul their entire system. This adaptability is crucial for long-term success, especially in the dynamic financial technology landscape where change is the only constant.

Additionally, these entities provide valuable domain expertise specific to regional markets, regulations, and payment methods. This specialized knowledge allows financial institutions to navigate local compliance requirements, understand consumer payment behavior, and optimize transaction flows more effectively. This can be especially beneficial for financial entities aiming to expand their footprint in geographically diverse markets.

Moreover, their solutions often come with robust analytics and reporting capabilities, offering actionable insights into transaction metrics, customer behaviors, and operational efficiencies. Such data-driven perspectives enable financial institutions to make more informed strategic decisions, refine their product offerings, and tailor their customer engagement strategies.

They also often provide value-added services, such as automated reconciliation, advanced fraud detection mechanisms, and even intelligent routing algorithms that optimize transaction pathways for cost-effectiveness and speed. Some even offer foreign exchange management tools that help financial institutions to mitigate currency risk and optimize cross-border transactions.

These companies are the unsung heroes of the payment ecosystem, providing the technological infrastructure and services that enable smooth and secure transactions. They play a vital role in enhancing the security, scalability, and interoperability of payment systems. As the payment landscape continues to evolve with emerging technologies and increasing regulatory scrutiny, the role of technical facilitators will become even more critical. Therefore, these entities are indispensable for the functioning and growth of today's global payment systems.