🔒 SEPA Instant cross-border

Demystifying SEPA instant across domestic borders

Welcome to The Engineer Banker, a weekly newsletter dedicated to organizing and delivering insightful technical content on the payments domain, making it easy for you to follow and learn at your own pace.

Want free access to the article?

25% off this Christmas!

Summary

This article provides a comprehensive overview of the evolution of SEPA Instant infrastructures across Europe. It delves into the details of the formation process, shedding light on how these infrastructures have developed over time. Additionally, the article explores the nuances of routing within both domestic and pan-European infrastructures, offering valuable insights into the path that instant transactions follow. Finally, it offers a detailed explanation of the TIPS settlement model, providing a holistic view of the entire SEPA Instant landscape.

Welcome to another episode of Realtime Infrastructures, where we take a deep dive into the intricate international routing mechanisms of SEPA Instant payments and explore the fascinating journey of an instant transaction as it traverses the diverse landscape of Europe's financial ecosystem. To comprehend this journey, we must first grasp the ever-evolving landscape of SEPA Instant in Europe today.

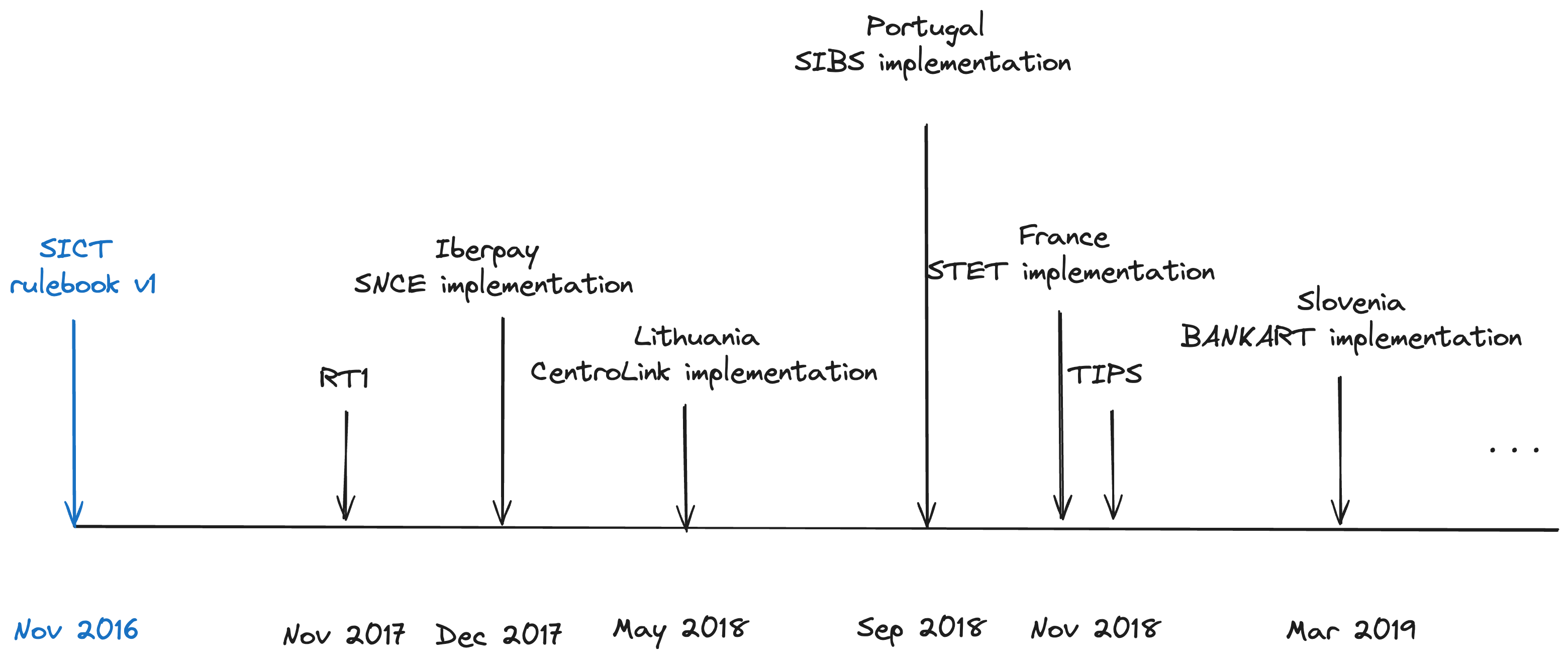

The inception of the SEPA Instant Credit Transfer (SCT Inst) scheme dates back to November 21, 2016, when the European Payments Council (EPC) officially released its pioneering rulebook. This momentous event heralded the birth of a groundbreaking system designed to seamlessly facilitate real-time euro (EUR) payments across the Single Euro Payments Area (SEPA). This foundational rulebook laid down the structural groundwork, offering a robust framework that allowed participating financial institutions to embrace and operationalize instant credit transfers within the SEPA zone.

The first SEPA Instant transaction was conducted by CaixaBank, a Spanish financial institution. CaixaBank made history by initiating the first SEPA Instant Credit Transfer (SCT Inst) transaction, marking a significant milestone in the adoption of real-time euro payments across the Single Euro Payments Area (SEPA).

Since its initial debut, the SCT Inst rulebook has undergone a series of meticulous updates and revisions. These ongoing refinements have been instrumental in elevating the scheme's capabilities, expanding its reach, and ensuring that it continues to meet the evolving needs of Europe's dynamic payments landscape.

In the wake of this landmark release, numerous nations and regions across Europe embarked on their individual implementations of the SCT Inst rulebook. Each implementation brought its unique nuances and adaptations to the framework, aligning it with the specific requirements and practices of the local financial industry. SEPA Instant Credit Transfer schemes were gradually being implemented by various countries within the Single Euro Payments Area (SEPA).

This is just a glimpse of the domestic implementations of SICT since its launch:

Spain: In Spain, the Spanish Payment System Operator (Iberpay) launched its SCT Inst scheme in December 2017.

France: France implemented its SCT Inst scheme in November 2018, led by the French Prudential Supervision and Resolution Authority (ACPR).

Lithuania: Lithuania's SCT Inst scheme was introduced in May 2018, coordinated by the Bank of Lithuania.

Slovenia: Slovenia adopted its SCT Inst scheme in March 2019, managed by the Bank of Slovenia.

Portugal: Portugal introduced its SCT Inst scheme in September 2018. The scheme was managed by the Portuguese Interbank Company (SIBS).

Simultaneously, the European Banking Association (EBA) initiated the development of a pan-European implementation in line with the rulebook. The RT1 (Real-Time 1) platform, operated by EBA CLEARING, was officially launched and made available to the public on November 21, 2017. RT1 is a pan-European infrastructure for processing SEPA Instant Credit Transfers (SCT Inst) in real-time, enabling financial institutions to offer instant payment services to their customers across the SEPA zone.

The European Central Bank embarked on the process of implementing its own version of the rulebook, adopting a pan-European approach as well. TIPS (TARGET Instant Payment Settlement) was officially launched and made available to the public by the European Central Bank (ECB) on November 30, 2018. TIPS is a real-time payment settlement system for instant euro (EUR) transactions, designed to enable financial institutions to settle payments in real-time, 24/7, across the Single Euro Payments Area (SEPA). TIPS was introduced to support the growing demand for real-time payments and to provide a pan-European solution for instant payments.

In the beginning, these domestic infrastructures ushered in real-time domestic transactions. Furthermore, they paved the way for the emergence of real-time person-to-person (P2P) payment methods, giving rise to innovative solutions such as Bizum in Spain and similar offerings in other jurisdictions. However, on the downside, this expansion led to a fragmented landscape, with numerous domestic implementations making the achievement of seamless European connectivity increasingly challenging. Those domestic implementations could only settle transactions between banks connected to the same CSM.

In one of our previous articles, we delved into the details of liquidity management within Ancillary System 6, particularly focusing on RT1. If you're looking to gain a deeper understanding of the liquidity management aspect within the SEPA Instant Credit Transfer (SICT) framework, it is recommended giving that article a read.

If you need a refresher on how the pacs.008 message is transported and utilized, consider reading these two informative pieces: